Hong Kong office rents expected to bottom out sooner than expected

Rents could decline by up to 5% next year.

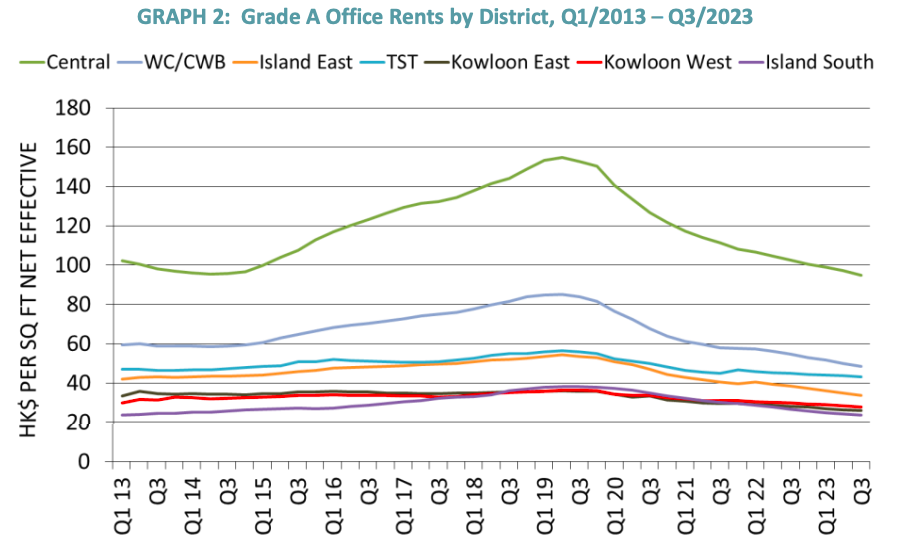

According to a recent report from Savills, the Hong Kong Grade A office rents experienced a 2% decline in Q3 2023. This can be attributed to shrinking demand in the market.

“However, it is worth noting that the vacancy rate also dropped by 0.4%. One of the factors contributing to this decline in vacancy is the imminent redevelopment of KITEC in Kowloon Bay, which has led to displacement demand as tenants seek alternative office spaces,” the report said.

Here’s more from Savills:

The market continues to be dominated by cost-saving moves, with landlords such as Wharf, Hysan, 3 Garden Road, and Hang Lung offering flexible leasing arrangements. These landlords are willing to provide capital expenditure for office units ranging from 2,000 sq ft to 4,000 sq ft. Moreover, these expenditures can be transferable to the next tenant, providing an attractive option for businesses seeking smaller office spaces. Some landlords are also assisting with renovation works, with the associated expenses being reflected in the monthly rent, typically adding HK$8 to HK$10 per sq ft.

While hardly a cost saving move, UBS previous committed to pre-lease 250,000 sq ft of XRL Topside Development in West Kowloon to consolidate their offices, currently mainly in Central, to this brand-new building on top of the high-speed rail. Most recently, it is reported that UBS would double the pre-committed spaces to 500,000 sq ft, or an entire tower of the four-block development, after its acquisition of Credit Suisse earlier this year. The actual relocation date is reported to be in phases after 2027, though.

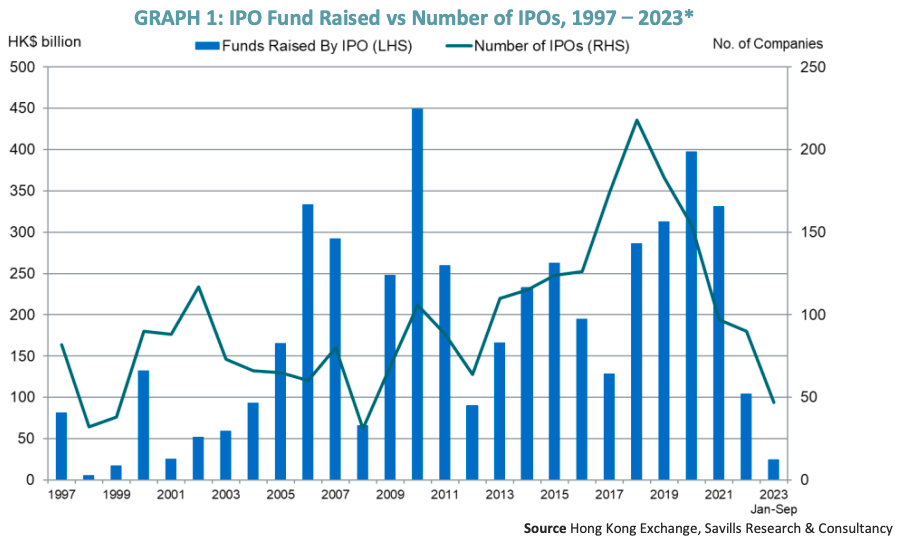

The IPO pipeline remained worrying thin with Q3 registering only 14 deals with HK$6.8 billion fund raised, as the stock market continued to tumble with HSI declining by another 6% over the quarter, and transaction volume also continued to shrink, with the HK$47 billion transaction volume on Oct 4 the lowest in five years. With only HK$24.6 billion raised so far this year, 2023 is bound to be the worst year for IPO since 2001, further dampening the already grim prospect of investment banks.

Despite the overall decline in demand, certain sectors have shown resilience in the Hong Kong office leasing market. Quantitative trading firms, which are known for their ability to generate profits even in challenging market conditions, have contributed to the demand. These firms are not restricted by geography and can trade in various markets. In addition, high-end retail sectors such as watches and art-pieces have remained stable compared to other retail sectors. The demand from these sectors has provided some support to the office leasing market.

Recently, The Office for Attracting Strategic Enterprises (OASES) signed strategic enterprise partnership agreements with twenty enterprises from various innovative industries, including life and health technology, artificial intelligence and data science, financial technology, and advanced manufacturing and new-energy technology. While these partnerships hold promise, the expansion of office spaces and demand from the innovation and technology (I&T) sectors remain uncertain. The market requires more concrete policies, incentive programs, and establishment timelines before feeling the full impact of these initiatives.

The Hong Kong office leasing market faces several headwinds and negative factors that could potentially accelerate its decline. Factors such as high interest rates, geopolitical tensions, and financial stress among Mainland corporates pose challenges to the market. These factors may lead to a bottoming-out process in office rents sooner than expected over the next year or two. Savills projects that office rents in Hong Kong will range from 0% to -5% in 2024.

Advertise

Advertise