Singapore private residential leasing volume underperforms 5-year average

The market declined by 2% YoY to 19,680 leases in Q1.

Savills Research shares that the private residential leasing market has contracted 2% on a year-on-year (YoY) basis, with 19,680* leases of private residential homes, excluding executive condominiums, inked island-wide in the first quarter.

This is 10.9% lower than the past five-year average of 22,084 transactions in the first quarter from 2019 to 2023.

The number of leasing contracts in the Rest of Central Region (RCR) decreased the most, by 6.4% YoY, this quarter. This is followed by the Core Central Region (CCR) with a YoY decline of 1.3%.

Rental contracts in the Outside Central Region (OCR) rose by 1.5% YoY, which is likely due to higher demand for more affordable homes, as well as a flux of new home supply, particularly in the second half of last year.

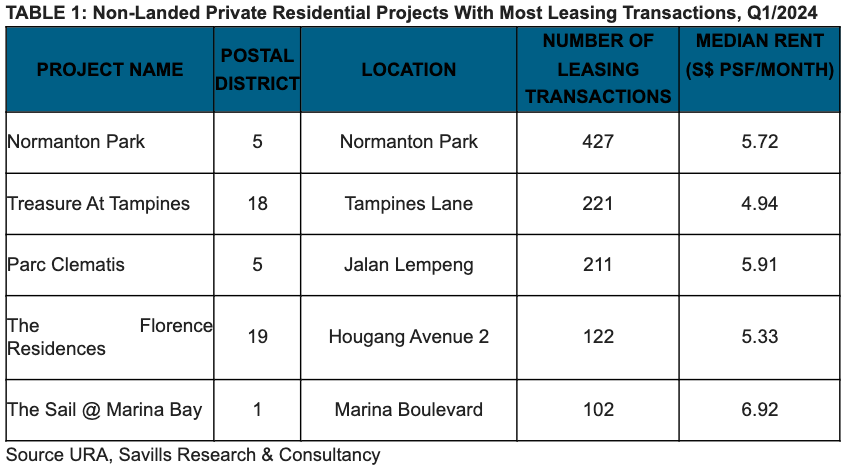

Top of the list of non-landed projects with the highest leasing contracts in Q1/2024 is Normanton Park with 427 leasing transactions. Two newly completed projects in the OCR – Treasure At Tampines and Parc Clematis – are in second and third places with 221 and 211 leasing transactions respectively. Rounding up the list are The Florence Residences and The Sail @ Marina Bay in fourth and fifth place.

Island-wide stock of completed private residential properties shrank to 410,400 units in Q1/2024, as just 241 private residential units received their Temporary Occupation Permits (TOPs) in the first quarter this year. Out of these, 200 units are from Meyer Mansion, a freehold condominium project located at Meyer Road in Marine Parade.

This has resulted in a sharp contraction from the last couple of quarters and is the lowest since Q2/2020 when only 86 units were completed. Coupled with the demolition of some units, this is the first time supply has dropped after housing stock has grown steadily for 3.5 years from Q3/2020.

The overall vacancy rate has improved by 1.3 percentage points (ppts) quarter-on-quarter (QoQ) to 6.8%. Vacancy rates has dropped across all the market segments: RCR recording the highest decrease of 1.5% QoQ, followed by the OCR at 1.4% QoQ and the CCR at 0.9% QoQ.

George Tan, Managing Director, Livethere Residential, Savills Singapore says, “Lately, feedback from the ground is indicating that agents are receiving more enquiries from younger singles or couples. This seems like another cycle building for a new batch of incoming professionals. Whether this is the beginning of another long cycle, or a short one remains to be seen because these enquiries could just be partially replacing the foreign professionals that had left. However, the feedback we have is not universally experienced by agents.”

Alan Cheong, Executive Director, Research & Consultancy, Savills Singapore adds, “It seems the rental market has turned from a landlord to a tenant’s market. If the feedback that another wave of younger professionals are arriving is true, it may support rents for room lettings or co-living premises. The number of leases signed for whole unit lettings should, however, remain soft as such lettings do not translate one-to-one to stamped leasing contracts. We still maintain our forecast of rents falling 5% YoY in 2024.”

*: Based on URA data

Advertise

Advertise