Why Singapore’s residential market is set for an extended bull run

Savills enumerates four key factors that contribute to the optimistic outlook.

Singapore’s private residential market is still on a roll and that roll doesn’t seem to have an ending soon, according to Savills, and this market momentum has brought to the fore some general observations. The analyst says these factors are likely to boost the longevity of the bull run.

These are:

- Reservoir of household wealth of the baby boomers;

- Underlying feelings across generations here towards private residential property;

- Foreign buyers’ perception of Singapore’s real estate market; and

- The distributed values of residential properties in general.

Here’s more from Savills:

We will begin by discussing the first two related points. For many years and across countries, the demand for housing has often been modelled using affordability models or housing value to income ratios. However, the strength of demand exhibited over the last 18 months pushes one to question whether such methods of measuring demand are appropriate.

Our frequent sounding of the state of the market from marketing associates reveal that for a few years already, a substantial number of buyers have been funded in part, especially the equity portion, by their parents. This cross generational funding makes it difficult for one to measure wealth levels here and the use of household income statistics become fuzzy if more buyers tap their parental savings, or parents voluntarily use their savings to buy a home under their children’s names.

While we cannot assess this type of household wealth and thus forecast how long this sort of demand will last, we realize that this phenomenon has only just begun and could last for a while. Graph 5 shows that the liquid assets per household has been rising faster than private residential prices (represented by the URA PPI). There are however no statistics of how this is distributed across age groups.

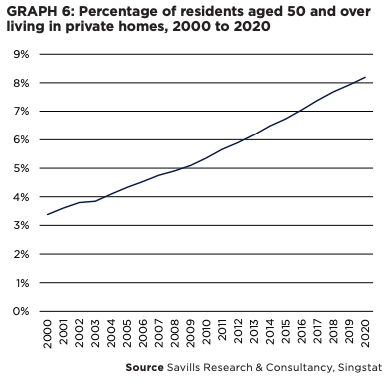

Graph 6 shows the number of Singapore residents aged 50 and older living in private housing. This sub-group has been increasing over time and is expected to continue rising until at least 2030.

Foreign buying of private residential properties has also been strong. This is despite the reversion towards more stringent pandemic measures in Q2/2021. Graph 7 shows that the top four buyers of non-landed private residential properties have in the past three quarters been a combination of nationalities with the Chinese dominating. In Graph 8, we see that amongst foreigners (excluding those unspecified foreigners) Chinese nationalities made up 25.6% of buyers, followed by Indonesians at 10.2% with the Malaysians and Americans each making up 8.4%. The interesting sub-group are the Americans which we believe will start to increase their share of foreign buying in the coming years. Amongst their high-networth individuals, the level of awareness of Singapore has been increasing over the years and this will correspondingly lead to stronger purchase numbers by them.

Notwithstanding the private residential market being caught up in a hive of activity in contrast with lethargic economic and job market growth, prices are still in sync with income distribution here. This should be good news because if housing values stray too far from income, then either policy intervention(s) or a rapid deflation of prices could torpedo the market’s buoyancy.

Concluding, we believe that while the fear of a wealth tax(s) being levied on residential properties may turn to reality one of these days, this is not likely to derail the long-term trajectory of residential property prices. If such a tax(s) is imposed, it will likely be a modification from one of the existing slew of cooling measures and re-labelled as a type of wealth tax. That would not have much of an impact as the market today appears comfortable with these cooling measures. Therefore, the top-down view is that for residential prices to mirror economic and social well-being, long term real estate prices should track median nominal GDP per capita growth. In the coming quarters, because of strong global inflationary tailwinds, nominal GDP is expected to rise above the real measure. This should help keep residential prices (both public and private) rising at above long-term averages.

Advertise

Advertise